Setting up multiple companies to separate business interests can seem very straight forward. There are however important considerations. We explore the implications of owning too many companies.

September 2023 Newsletter

20 September 2023

Accounting & Compliance, Ambitious Startups, Building a Business, Reducing Tax, Selling a Business, Structuring a Business

Back to school – set up a tax-free childcare account?

The Government’s Tax-Free Childcare Accounts provide a 25% subsidy towards the cost of childcare.

The account can be used to pay nursery fees, breakfast clubs, after school clubs and registered childminders.

How does the Scheme work?

The scheme operates by topping up savings of up to £8,000 per child by 25%, potentially an extra £2,000 a year from the Government to spend on qualifying childcare.

The scheme generally applies to children under 12.

In the case of disabled children the age limit is 16 and the amount that can be saved is £16,000 a year, topped up by the Government by a further 25% to potentially £20,000.

Unlike childcare vouchers, still provided by some employers, tax free childcare accounts are available to both employees and the self-employed.

Am I Eligible?

To be eligible, the parent generally needs to be working and earning at least the National Minimum Wage or National Living Wage for at least 16 hours a week on average.

However, parents are not eligible if either of the parents’ adjusted net income is more than £100,000 a year.

Note that where an employer provides Childcare Vouchers then the parents are not allowed to set up a Tax-Free Childcare Account as well.

Should I leave my employee Childcare Voucher Scheme?

Please contact us for advice on whether or not it would be beneficial to leave your employer’s Childcare Voucher Scheme, noting in particular that the voucher scheme applies to children up to age 16, rather than age 12.

I have a high income – what happens to my entitlement?

If you’re also concerned about losing your entitlement to pay into a tax free account due to your income exceeding £100,000, then please get in touch to discuss your options – pension contributions aren’t just useful for reducing the tax you pay at the higher rate, but also for preserving your childcare account entitlement!

Child Benefit May Create A Tax Charge For Those With High Income

Parents and carers need to be aware that if either of the couple have ‘adjusted net income’ in excess of £50,000 then the one with the higher income will potentially be charged to tax on some or all of the child benefit and will need to request a self-assessment tax return to report the amount of child benefit received in the tax year.

How long has HICBC existed?

The High Income Child Benefit Charge (HICBC) was introduced in 2012/13 and imposes a 1% charge on the amount of child benefit received for every £100 that the taxpayer’s adjusted net income exceeds £50,000.

What is my “Adjusted net income?”

‘Adjusted net income’ is an individual’s total taxable income before any allowances, but after deducting Gift Aid, pension contributions, and trade union subscriptions.

Where the adjusted net income is £60,000 or more, then 100% of the child benefit is charged, effectively fully clawing back the child benefit.

Note that the £50,000 threshold has not been increased since it was introduced in 2012 which means that more and more parents are being caught by the HICBC each year.

It has recently been announced that in future years the government plans to deduct HICBC directly from salaries via PAYE.

Can I opt out of Child Benefit?

It is possible to opt out of receiving Child Benefit payments where adjusted net income exceeds £60,000.

Consequently, the HICBC would not apply and the child benefit would not need to be reported on the tax return.

That may mean that a taxpayer who has their tax collected under PAYE would not be required to submit a self-assessment tax return.

It is important to still fill in the Child Benefit claim form but state on the form that you do not want to get payments.

That is important as the claimant would then receive National Insurance credits for that year, which count towards their State Pension entitlement.

What do I need to be aware of?

One of the problems with the HICBC is that those taxpayers who pay their tax under PAYE are not normally required to file a self-assessment tax return.

However, if they are parents and one of the couple is in receipt of child benefit then they are required to request a self-assessment tax return from HMRC to report the child benefit if their adjusted net income exceeds £50,000 a year.

Previous tax years

We have seen that HMRC have started assessing taxpayers to HICBC where they have not reported their child benefit in earlier years.

Several taxpayers have successfully challenged these assessments through the courts in a number of recent tax cases.

Whether or not a successful appeal can be made will depend on the circumstances in each case.

If you’re concerned any of the above applies to you then please get in touch with your account manager to discuss; as always it’s much better to approach HMRC before they approach you!

Pay back criteria

HICBC is widely regarded as an unfair charge, due to the pay back criteria.

For example, say you have a dual income household with both parents earning £50,000 – their total household income is £100,000 and they don’t need to pay back any child benefit.

On the other hand, say you have a single income household, with one parent earning £60,000 – now their household income is £60,000 and they lose full entitlement to child benefit!

There have been calls for a number of years to revise the HICBC, however HMRC are yet to make any changes!

Merger Of R&D Tax Relief Schemes To Go Ahead

The government have issued draft legislation for consultation on the proposal to merge the two forms of corporation tax relief for expenditure on research and development (R&D)

The Proposal

For expenditure incurred on or after 1 April 2024, it is proposed that the two schemes providing for R&D relief – R&D expenditure credit (RDEC) and Credit Relief for SMEs, will be merged and replaced with a single unified scheme.

This will operate alongside a new scheme to provide additional relief for “R&D intensive” SME companies.

How will this operate?

It is suggested that this merged scheme will operate in a similar manner to the existing RDEC scheme, rather than the SME scheme.

The merged scheme will offer a taxable credit, based on a percentage of R&D expenditure, that can be offset against the company’s tax liability.

The rate of relief under the proposals is 20% of R&D expenditure.

This translates into a net benefit of 15%, assuming a company pays tax at the 25% main rate of corporation tax.

Exceptions

The exception to this would be for loss-making “R&D intensive” SMEs.

These companies would be able to continue to claim an additional deduction for R&D expenditure, and where that deduction produces or contributes to a loss, claim a payable credit for that loss.

“R&D Intensive” SME companies

It is envisaged that the current SME relief will effectively continue for loss-making R&D intensive companies.

What is R&D Intensive?

An R&D intensive company is broadly defined as being where R&D expenditure is 40% of the company’s total expenditure for the purposes of calculating profits chargeable to corporation tax.

For those companies, the additional deduction will remain at 86%, with the rate of payable credit for surrenderable losses being 14.5%.

This would provide a repayable credit of £26.97 for every £100 spent on qualifying R&D.

R&D has been the subject of a flurry of changes in recent months and it is often a minefield to navigate the qualifying criteria and claim rules; not to mention HMRC have really clamped down on R&D claims recently in order to tackle the increasing number of fraudulent claims.

Are you eligible to claim?

If you’re undertaking any projects that you believe might qualify then please get in touch and we can assist on advising and completing the claim.

Also, if you’ve been approached by a third-party company about a potential R&D claim, then please contact us.

We can explore the legitimacy of whether your claim will qualify for tax relief to ensure you’re fully compliant with HMRC rules.

Income Tax On Inherited Pension Funds

Currently, where an individual pension holder dies before age 75, drawdown pensions paid to a successor can generally be received free from income tax.

Where the pension holder dies over the age of 75, then the amounts drawn by the successor are taxed at their marginal income tax rate.

Note also that the current tax rules provide that the value of the fund passes free of inheritance tax to the successor and thus forms an important part of estate planning.

Draft Legislation

Policy documents published in July 2023 include draft legislation to abolish the pension lifetime allowance and associated income tax charge.

These were previously announced as part of Budget Day measures to lure workers aged over 50 back into work and are generally welcomed.

However, the policy documents regarding changes to the taxation of pensions also included a suggestion that certain beneficiaries of pensions of members who died under age 75 may become subject to income tax as part of future tax changes, possibly from 2024/25.

This would align with the tax position for beneficiaries of pensions where the member dies over age 75.

Later life Planning Strategies

Pension planning and inheritance tax are often overlooked by many taxpayers who have more focus on the ‘now’, however these are two areas that can be very costly if not planned well.

If you’re interest in active pension planning, not only to reduce your yearly tax bill but also to provide for a comfortable retirement, then please get in touch!

We have a team of tax experts as well as pension advisors at our sister company Friend & Grant Wealth Management that can help you.

HMRC To Require More Information To Be Provided By Taxpayers

Draft legislation released for consultation on 18 July indicates that business and individual taxpayers will be required to provide more information to HMRC in the next few years.

Increased Reporting

It is proposed that from 2025/26, employers will be required to provide more detailed information on employee hours worked via real time information (RTI) PAYE reporting.

The information to be reported will be set out in separate regulations.

Shareholders

From 2025/26 shareholders in owner-managed businesses will also be required to provide additional information via their self- assessment tax returns.

These shareholders will be required to disclose the amount of dividends received from their own companies separately from other dividend income, as well as the percentage shareholding that they hold in their own companies.

Self-Employed

Self-employed individuals will be required to provide information on the start and end dates of their businesses via their self-assessment returns.

How will this affect me?

For the most of our clients, these proposed changes should not prove a burden as we already have much of the information.

Where the extra work lies is with the payroll for employees – effective records will need to be kept by businesses to keep track of employee working hours and be effectively communicated with either our payroll team or your internal payroll team.

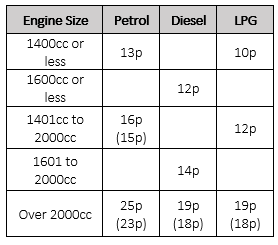

Advisory Fuel Rate For Company Cars

The table below sets out the HMRC advisory fuel rates from 1 September 2023.

These are the suggested reimbursement rates for employees’ private mileage using their company car.

Where the employer does not pay for any fuel for the company car these are the amounts that can be reimbursed in respect of business journeys without the amount being taxable on the employee.

Where there has been a change the previous rate is shown in brackets.

You can also continue to use the previous rates for up to 1 month from the date the new rates apply.

Not Diesel or Petrol?

Note that for hybrid cars you must use the petrol or diesel rate.

For fully electric vehicles the rate is 10p (9p) per mile.

Getting Reimbursements right.

As an employer, its important to get it right when reimbursing employees for any expenses.

For company cars, if fuel is reimbursed at a rate higher than the above then the excess is taxable on the employee as earnings.

If you or and employee is undertaking business travel in a personal vehicle instead of a company car, then the applicable rate is 45p per mile up to 10,000 miles and 25p per mile thereafter.

The content in this blog is correct as at 20th September 2023. See terms and conditions.