Setting up multiple companies to separate business interests can seem very straight forward. There are however important considerations. We explore the implications of owning too many companies.

June 2023 Newsletter

6 June 2023

Accounting & Compliance, Building a Business, Reducing Tax, Structuring a Business

2022/23 Employment-Related Securities Returns Due By 6 July

The deadline for reporting shares and securities and share options issued to employees for 2022/23 is 6 July 2023. This is the same as the deadline for reporting expenses and benefits provided to employees on form P11d for 2022/23.

Employers must submit their employment related securities annual returns online and attach the appropriate spreadsheet template if they have something to report. HMRC provide templates on their website that may be downloaded in order that the information may be entered and uploaded.

Note that there are different templates for each of the four tax-advantaged employee share schemes –

- Company Share Option Plan (CSOP)

- Enterprise Management Incentives (EMI)

- Save and You Earn (SAYE) share options

- Share Incentive Plans (SIP).

In addition, spreadsheet 42 should be used to report any other employment-related securities (non-tax-advantaged) issued to employees and directors.

Need assistance?

We can of course assist you with the completion of the reporting obligations and with the valuation of the securities concerned.

We have completed all Employer Related Securities Returns for share transactions we are aware of for our clients, however if you have not been contacted and believe you may need to file, please contact Christie Inns.

HMRC Official Rate Of Interest Only 2.25%

HMRC have announced that the official rate of interest will increase from 2% to 2.25% on 6 April 2023.

The official rate of interest is used to calculate the income tax charge on the benefit of employment related loans and the taxable benefit of some employment related living accommodation. These rates used to fluctuate in line with the base rate, but in recent years HMRC has fixed the rate for the whole tax year.

For those employers including beneficial loans on form P11d for 2022/23 the average official rate to be used is 2%.

The charge applies where the amount of the loan exceeds £10,000.

How does HMRC’S official rate of interest affect directors?

The HMRC rate of interest on beneficial loans looks very attractive compared to the Bank of England Base rate of 4.5% and much higher rates charged by banks for unsecured loans.

Note that where loans are made to participators (broadly shareholders) of a close company there is potentially a special tax charge on the company on any loan still outstanding 9 months after the end of the accounting period, this is called Section 455 tax or S455 for short.

The charge is currently 33.75%, the same as the higher rate of tax on dividend income.

This tax charge is only repaid to the company when the overdrawn director’s loan is repaid or written off.

For Example

Fred, the managing director and controlling shareholder of Bloggs Ltd, is loaned £100,000 interest free on 6 April 2023.

No repayments are made in the year ended 31 March 2024.

Assuming no change in the HMRC official rate of interest the company would show a taxable benefit in kind on Fred’s 2023/24 P11d of £2,250 (2.25%).

Repaid in full

If Fred repays the loan in full before 31 December 2024 there would be no special charge on the company although Fred would be assessed on the beneficial loan for the 9 months that the loan was in existence in 2024/25.

Note that there are anti- “bed and breakfast” rules to counteract the situation where the loan is readvanced by the company.

The anti-avoidance would not apply where the loan is cleared by crediting a bonus or dividend to Fred’s loan account.

Partial Repayment

If however only £60,000 was repaid by Fred before 31 December 2024 leaving £40,000 outstanding, then there would be a S455 charge on the company of £13,500 (assuming 33.75% continues) which would be payable in addition to the company’s corporation tax liability for year ended 31 March 2024.

The company would show a taxable benefit in kind on Fred’s 2024/25 P11d based on the official rate of interest on beneficial loans for 2024/25 (yet to be determined).

Please note that a taxable benefit in kind would not arise if the company charged interest equivalent to the official rate of interest on the loan.

Waive/Write off outstanding loan

If the company then decides to write off or waive the outstanding loan in year ended 31 March 2025 the £13,500 would be refunded.

However, Fred would be assessed on the £40,000 as an income distribution (dividend) arising at the date of waiver in 2024/25.

Tax Efficient Profit Extraction

Our aim is to work with our clients in order to achieve for them the most tax efficient method of extracting profits from their company.

If you’d like to discuss remuneration options or have a tax planning meeting to effectively plan your tax affairs, please contact your account manager.

Should employees reimburse their employer for private fuel?

Where the employer provides an employee with a company car there may be an additional benefit in kind on the provision of fuel for private journeys which needs to be reported on form P11d.

This additional benefit is based on a notional list price for the vehicle of £25,300 for 2022/23 which applies irrespective of the original list price of the vehicle normally used to compute the taxable benefit.

That figure is then multiplied by the CO2/km percentage for that vehicle.

For example

A Range Rover Evoke S AWD Automatic MHEV has a current list price of £41,245.

The CO2 emissions data on the Land Rover website is 168g/km for this vehicle. which means that the fuel benefit is 37% multiplied by £25,300 = £9,361.

For a higher rate taxpayer that would result in a tax liability of £3,744.

That would be an awful lot of fuel!

In addition, the employer would have a Class 1A national insurance liability of £1,360 (14.53% for 2022/23).

Private fuel that is reimbursed

Provided private fuel is fully reimbursed, the fuel benefit does not apply.

This is an all or nothing benefit and unless there is full reimbursement there is an additional taxable benefit.

The deadline for reimbursing private fuel is 6 July 2023 for the 2022/23 tax year.

Tax Planning for your company vehicle

Company vehicles can provide great tax benefits but can also be costly if not planned effectively.

If you’re thinking of purchasing a company vehicle, please contact your account manager to discuss the tax consequences beforehand.

The make and model and financing type can all have varied affects on the personal tax and corporation tax impacts of the purchase, so we suggest seeking advice prior to purchase to ensure you’re being as tax efficient as possible!

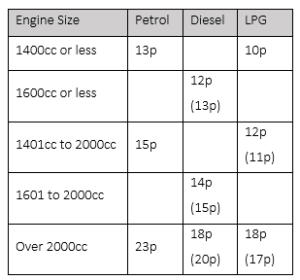

Advisory Fuel Rate For Company Cars

The table below sets out the HMRC advisory fuel rates from 1 June 2023.

These are the suggested reimbursement rates for employees’ private mileage using their company car.

Where the employer does not pay for any fuel for the company car these are the amounts that can be reimbursed in respect of business journeys without the amount being taxable on the employee.

Where there has been a change, the previous rate is shown in brackets.

You can also continue to use the previous rates for up to 1 month from the date the new rates apply. Note that for hybrid cars you must use the petrol or diesel rate. For fully electric vehicles the rate is 9p (8p) per mile.

A word of caution

If an employer reimburses fuel at an amount higher that the advisory rates above, then the excess needs to be reported through PAYE and is subject to tax and national insurance as if it were additional earnings.Please contact your account manager if you have any queries regarding company cars and reimbursing fuel or mileage.

Use Of HMRC Advisory Rates For VAT Purposes

Where employers reimburse their employees for using their own cars for business journeys the tax – free reimbursement rate continues to be 45p for the first 10,000 business miles and 25p a mile thereafter.

There is also an additional 5p per mile per passenger.

These rates have not increased for about 10 years!

Provided the employee provides a fuel receipt from the filling station the employer is able to reclaim input VAT on a portion of the amount reimbursed to the employee.

The input VAT is 1/6th of the advisory fuel rate for the employee’s vehicle.

Keep hold of invoices and receipts

When completing your VAT Returns it’s always important to ensure you’re keeping all invoices and receipts as evidence – in the event of a HMRC enquiry, the officer would request to see certain ones.

If you’ve got any queries on the above then please contact your account manager.

The content in this article is correct as at 6th June 2023. See terms and conditions.